Premium Coverage for Your Hot Takes

Talking online becomes an insurable risk

The Janky Time Machine’s chronometric phase array decided to interpret “a little ways forward” as “somewhere that requires multiple forms of identification,” and I ended up in a co-working space that smells like anxiety and cold brew. The temporal stabilizers are making a grinding noise that the repair manual describes as “cosmically inconvenient,” so I’m stuck here until the chronometer decides to cooperate.

Found this card tucked into someone’s wallet at the hot-desk next to me—right between their transit pass and what appears to be a coffee shop loyalty program, except this one tracks your “daily authentic human interaction quota.” But that’s another post.

Here’s what nobody tells you about the professionalization of everything: once you start requiring credentials to talk about medicine or finance online, someone’s going to start selling insurance for when you inevitably say the wrong thing anyway. And once there’s insurance, there’s tiers. And once there’s tiers, there’s people who can afford to speak and people who can’t.

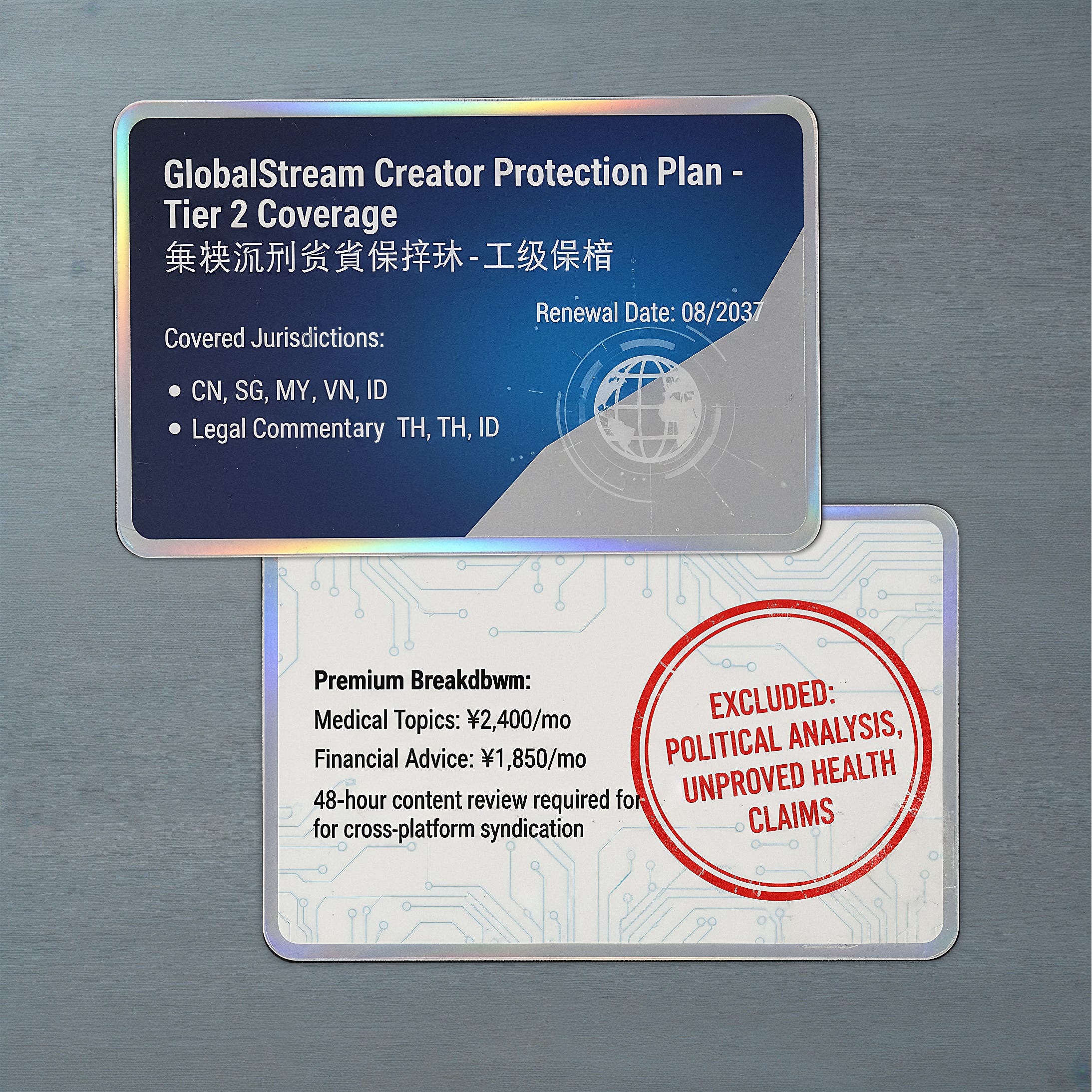

¥2,400 per month1 to discuss medical topics. That’s not a typo. That’s what it costs to maintain the right to give advice about which tea is good for a cold or whether your back pain might be serious. Financial advice is slightly cheaper at ¥1,850—which is ironic, because one piece of bad financial advice is how you end up unable to afford the insurance that lets you give financial advice. It’s a very tight feedback loop.

Back in my primeline, most influencers doling out health tips are sick and the ones giving financial advice are broke. They don’t have credentials—they have affiliate links. Somehow we went from “completely unqualified but free” to “properly credentialed and prohibitively expensive” without ever stopping at “maybe let’s just think about this for a second.”

Legal commentary sits at the premium tier, ¥3,100 monthly. Meanwhile, political analysis isn’t just expensive—it’s straight-up excluded. That big red “EXCLUDED” stamp doing a lot of quiet work there.

The 48-hour content review requirement is maybe the most telling. You don’t just insure your speech, you pre-clear it. The bureaucracy doesn’t trust the insurance, the insurance doesn’t trust you, and somewhere in between, the idea of spontaneous public conversation became a liability nobody can quite afford to underwrite.

The temporal coolant is now pooling around my feet, which is definitely going to affect my deposit. The co-working space has a sign about “uncontained temporal fluids” and a fine schedule I can’t afford.

But I keep staring at those jurisdiction codes: CN, SG, MY, VN, TH, ID. Six countries where your words need liability coverage before they cross a border. Makes you wonder what the maps look like for everyone who can’t afford Tier 2 protection. Or what happens to all the conversations that used to be free, back when talking was just talking and not a cross-border financial instrument requiring monthly premiums and pre-publication review.

Guess that’s what we mean now when we say someone’s “uninsured.”

The Janky Time Machine finally stopped leaking. Unfortunately, it’s because all the coolant is now on the floor. If anyone knows a good temporal mechanic who works pro bono, my coverage doesn’t extend to equipment malfunctions.

Today’s entry is inspired by China’s new rules requiring ‘influencers’ to be credentialed to talk about certain topics. Is it too heavy-handed? Maybe. Do I disagree with what they’re doing? Maybe … not? What do you think?